Vol. XXVI, No. 5, May 2026

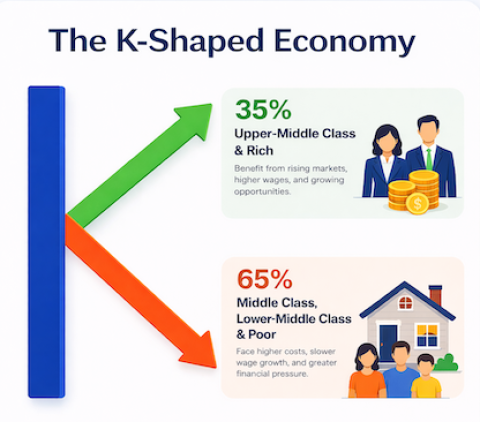

The K-shaped economy and its impact on location-based entertainment

What is a K-shaped economy? Simply put, the U.S. economy is becoming increasingly more bifurcated. Higher‑income, asset‑owning households are seeing incomes and wealth grow, maintaining their spending, while many middle- and lower-income households are struggling with weaker income gains and inflation, so they are cutting back on unnecessary spending. Instead of a broad, stable middle class, more people are clustered at the top and bottom.

But a K-shaped economy isn't new. It's a continuation of a long-term trend of expanding inequality in America. Today, the K-shaped economy is more split than ever due to what some commentators call an affordability crisis.

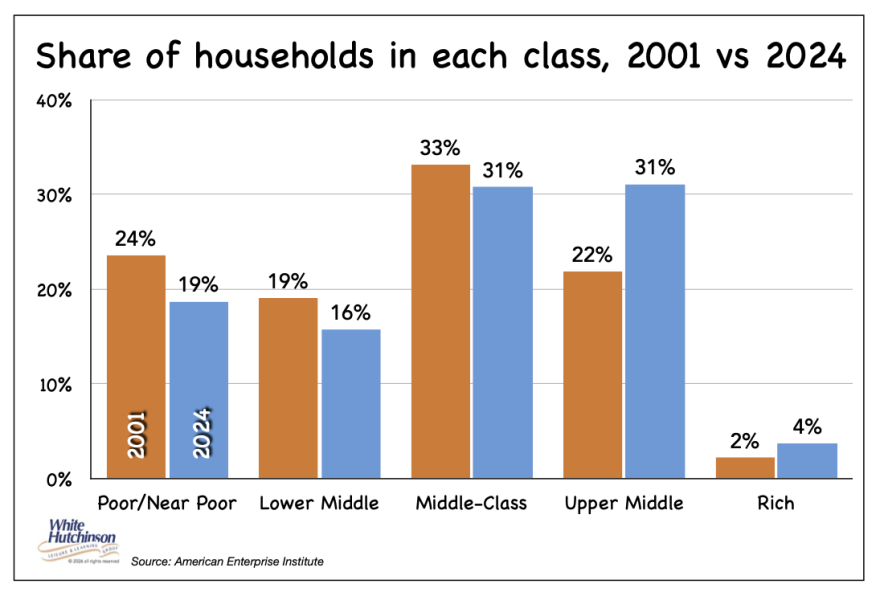

New research from the American Enterprise Institute shows that the ranks of the affluent have grown markedly over the past several decades, while the lower rungs of the middle class have shrunk. In 2024, about 31% of Americans were part of the upper middle class, up from about 22% in 2001.

The AEI report divided families into five income groups - poor, lower middle class, core middle class, upper middle class, and rich. The report found that 35% of households now fall into the two highest-earning groups, upper middle class and rich, while fewer fall into the three lower-earning categories.

The report's analysis used the federal poverty guidelines to determine which group a family fell into. The report classified a three-person family earning between five and 15 times the poverty guideline as upper-middle class, or between $133,000 and $400,000. In 2024, the rich were considered to be earning $400,000+. The core middle class was considered to be earning between $67,000 and $133,000 for a family of three.

The core middle class shrank from 33% of families in 2001 to 31% in 2024, while the upper-middle class grew from 22% to 31%. Together, the upper-middle class and the rich ($133,000+ incomes) grew from 24% in 2001 to 35% in 2024. They are in the upper part of the K-shaped economy, while 65% of families are in the lower part. This is exactly the “K‑shaped” pattern: more at the top, taking a growing share of income and accounting for a greater share of discretionary spending.

A Pew Research Center analysis using a different methodology also found that the share of American families in the higher-income group is increasing.

A February 2026 Bank of America report found a widening gap in spending growth between the two legs of the K-shaped economy starting in mid-2025. As of February 2026, year-over-year growth in spending among the highest third of income households exceeded inflation, while growth in spending by the lower two-thirds was below inflation, partly due to weaker wage growth that limited their ability to spend on discretionary categories. Their data showed that wealthy consumers are still increasing non‑essential spending (premium services, and experiences) while lower‑ and middle‑income households are hunting for discounts and cutting back on discretionary categories.

A report this month by the Federal Reserve Bank of New York found that spending has exhibited a K-shaped economy since 2023, driven by high-income households' (those earning more than $125,000 per year) spending growing at a faster rate than lower-income households.

The K-shaped economy is reshaping the landscape for location-based entertainment (LBEs), including family entertainment centers (FECs). Rather than a broad middle-class consumer base rising or falling together, we now see one segment of middle-income households pulling ahead while another struggles with stagnant wages and rising costs. It's a bifurcated world. The split shows up directly in who visits LBEs/FECs, how often they come, and how much they spend.

For LBEs and FECs, this means the average middle-class consumer is no longer the core customer. A more affluent segment of the market still has money for travel and premium out-of-home experiences. Meanwhile, a large share of families is trading down, reducing visit frequency, spending less when they do attend, or dropping out of the market altogether.

LBEs and FECs that look and feel like just another generic amusement center and pizza joint are under the most pressure. In a K‑shaped world, the middle LBEs/FECs get squeezed. They are neither cheap enough for the budget‑conscious nor special enough for high-income customers.

Legacy FECs were designed for a world where:

- The middle class was larger and expanding.

- Households with children were more common.

- Parents prioritized kid‑centric activities as a primary leisure category.

The K‑shaped economy compounds deeper trends that were already undermining the legacy FEC model:

- Fewer households with children in the core 5-14 age group in many markets mean a smaller natural audience for child‑focused centers.

- Parents are more likely to prioritize experiences they enjoy - social activities, good food, curated drinks, and stylish environments - and bring kids along, rather than choose activities that only kids enjoy.

- Upscale, competitive socializing and social game eatertainment venues that primarily target adults and combine interactive group activities and games with high-quality food, drinks, and atmosphere are drawing demand and revenue away from legacy FECs.

As a result, many legacy FECs are stuck in the squeezed middle. They are neither cheap enough for value‑seekers nor distinctive enough for higher‑income guests, so they are seeing flat or declining visits, greater price resistance when they try to offset costs, and a widening quality gap versus newer, more adult‑oriented competitors.

Households on the upper arm of the K, those with high incomes and assets, behave differently:

- They are still spending on experiences including travel, concerts, premium dining, high-quality out-of-home entertainment, and transformative experiences.

- Expectations on quality, theming, tech, and F&B have risen. Higher‑income guests compare LBEs/FECs to premium dining, travel, and live events, not just other amusement centers, making good‑enough centers non‑

- They are more selective. If they're going to use their limited discretionary leisure time, they want the experience to feel elevated, with thoughtful design, quality food and beverage, service that respects their time, and social “brag‑”

- They are less price‑sensitive on the margin: they will pay more for higher‑quality, flavor‑forward food and drink, and for special events, as long as the perceived value is high.

This higher socioeconomic segment naturally supports the new paradigm concepts:

- Premium competitive socializing and social game eatertainment venues

- Advanced attractions such as VR and immersive experiences

- Strong food and beverage programs (craft cocktails, curated beer, scratch kitchens, craveable and elevated comfort bar fare with familiar flavors as well as global and street food inspired options, etc.).

They are much less interested in dated, fluorescent‑lit, noisy middle-of-the-road family entertainment centers with mediocre food, even if those centers offer modern attractions and games.

On the bottom side of the K, households under budget pressure are:

- Reducing frequency: visits become special‑occasion events rather than regular weekly or monthly routines.

- Focusing on value: clear, predictable pricing and “all‑in” offers that control the total check are critical.

- Trading down: substituting free or low‑cost community events, at‑home entertainment, and streaming, which directly compete with LBE/FEC visits.

In other words, price sensitivity is high, and tolerance for upscale experiences at premium prices is very low.

The rise of competitive socializing and social game eatertainment, including duckpin and boutique bowling, interactive darts, archery‑style games, and other social games, fits today's K‑shaped reality well:

- They attract higher‑income young professionals and corporate groups who are still spending, particularly on weekdays.

- They generate strong F&B per‑capita and can support premium pricing for games/bays and events.

- They remain accessible to middle‑income guests through off‑peak pricing, shareable plates, and a fun, non‑intimidating environment.

For LBEs/FECs, this points to a strategic evolution from kid‑centric with some adult tolerance to adult‑centric with some family‑compatible options, especially in suburban markets with sufficient upper‑middle‑ and affluent‑households.

Consumers in the upper leg of the K expect higher-end finishes and atmosphere. Here are two examples of centers that meet those standards. At the top is F1 Arcade and at the bottom, Ocean5 designed and produced by White Hutchinson Leisure & Learning Group.

Putting it all together, operators should move beyond generic family fun toward adult-social and family-compatible offerings, with upscale ambiance and service, and make F&B a true profit center. Treat the menu, bar, and service as central to the experience, not an afterthought.

In short, the K-shaped economy is amplifying an old marketing adage. LBEs/FECs cannot win by trying to be all things to all people and with a middle-of-the-road offering. Success now comes from understanding the K-shaped economy and targeting upper-middle- and higher-income families as the primary market, with facilities and offerings that align with their tastes and expectations.

Next month, we will discuss a barbell strategy to capture the top of the K while also reaching some of the middle market.

Subscribe to monthly Leisure eNewsletter