Vol. I, No. 2, April 2023

Do you know your cost of goods sold percentage?

Cost of goods sold (COGS) percentage is one of the most important financial performance metrics for foodservice. Without constantly calculating and monitoring the COGS percentage, it is impossible to determine the profitability of different food and beverage items and whether you are making a profit. Constant monitoring of COGS percentages allows you to catch problems before they multiply into significant lost profits.

For a foodservice operation, COGS is the percentage cost of all food and beverages consumed during a period of time. Typically, COGS is calculated weekly.

COGS is calculated using this formula:

(Beginning Inventory + Purchases) - Ending Inventory = COGS

The beginning inventory means the amount of food and beverage in the kitchen and storage areas at the beginning of a period, usually at the beginning of the week. For instance, if on Monday, there is $6,000 worth of food and beverages on hand, then $6,000 is the beginning inventory.

Purchases mean the amount of food and beverages purchased and delivered that week. If deliveries of $4,000 worth of food and beverages arrived that week, that would be the purchases.

Ending inventory is the amount of food and beverage products left at the end of the week. Although the product was purchased and delivered during the week, there will be less inventory at the end of the week since food and beverage were sold, discarded, or disappeared (probably theft) during that week. So, if inventory is taken the following Monday and $4,000 worth of inventory remains, that is the ending inventory (It is also the beginning inventory for the next week).

In the above, the foodservice facility had $6,000 worth of inventory on hand on Monday and purchased another $4,000 of food and beverage products that week, for a total of $10,000 worth of inventory. The following Monday morning, there was $4,000 worth of inventory remaining. This means that $6,000 worth of inventory was used or disappeared, the COGS for that week.

($6,000 + $4,000) = $10,000 - $4,000 = $6,000 COGS

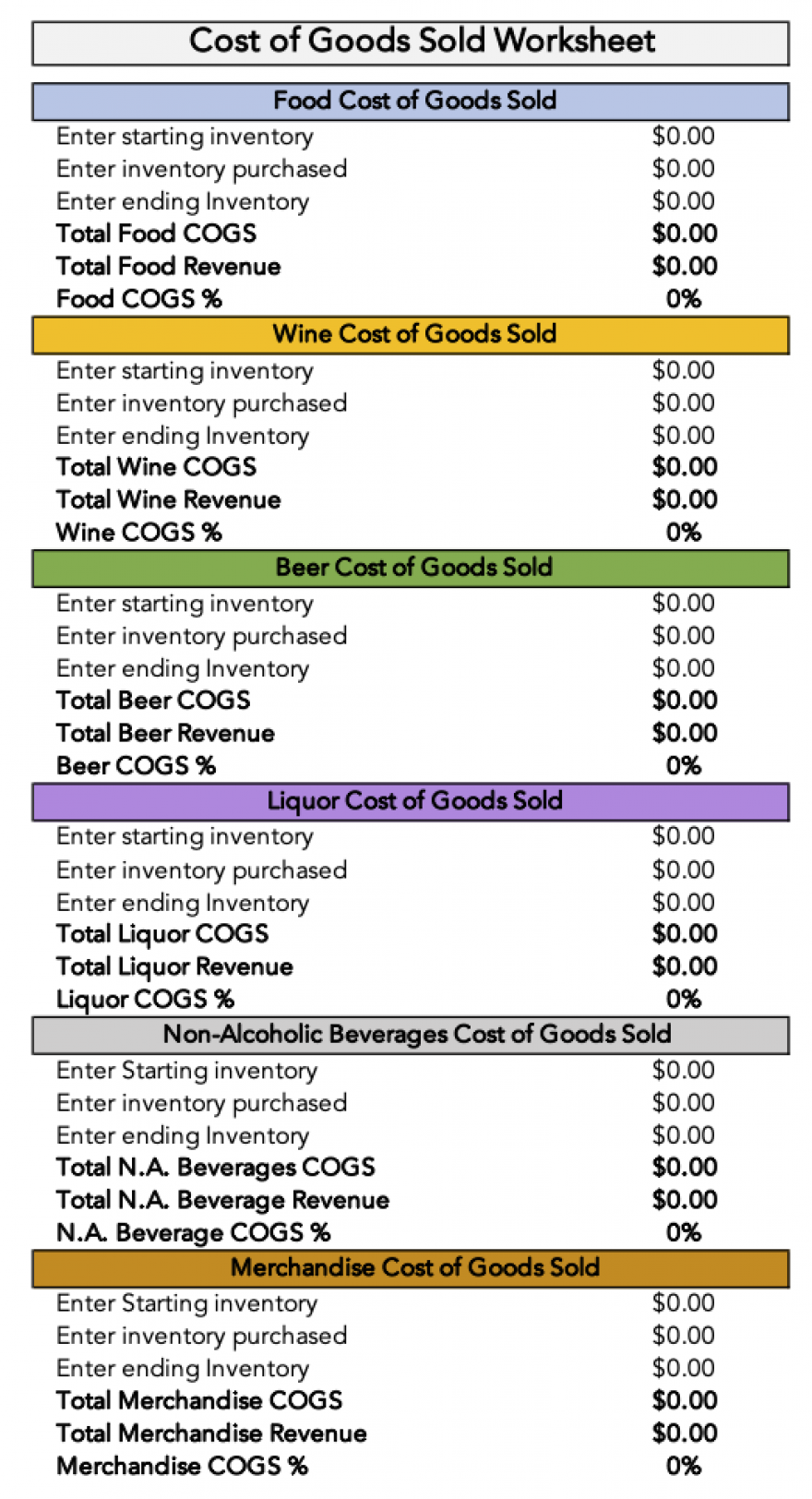

Rather than compute COGS for all food and beverage together, it is important for profit management to calculate COGS for different categories of F&B. Food and different beverages will have different target COGS, so it is important to calculate them individually. Typically, it is calculated separately for food, beer, wine, liquor, non-alcoholic beverages, and merchandise sales. That is important so the target COGS percentages for each can be monitored.

COGS percentages are determined by dividing the COGS by the revenue. For example, if the COGS for beer that week was $1,000 and $4,000 of beer was sold that week, the COGS percentage for beer would be 25%.

COGS divided by Revenues = COGS Percentage

If any COGS percentage is too high, then an investigation should be made to determine and correct the problem, which could include things such as incorrect portion control, product price increases, excessive waste, and even theft.

In the restaurant industry the rule of thumb target COGS percentage for food is around 30% and for alcohol, around 25%. For agritourism farms, lower overall COGS percentages of 25% or less can be achieved for food due to the mix of many high margin items (kettle corn, donuts, etc.). For liquor, the typical target COGS is between 18% and 24%. For draft beer it's around 18%. Bottled beer is 24% to 28% depending on the mix of domestic and imported beers.

Below is a worksheet template for all these calculations. You can download the Excel worksheet with all the formulas built in by clicking here.

Click here to download Excel worksheet

Subscribe to Agritourism Today